Race to Space: A deep dive into Space-related SPACs

With the recent NASA Mars Rover landing, the mission of making humanity a multi-planetary species seems more achievable than ever before. The excitement around space exploration has aptly translated into the public equity markets, as space-related companies have seen their stock prices surge throughout the past few months.

Not surprisingly, SPAC sponsors have jumped at this opportunity by bringing young space companies public through this route. Some of the recent deals in this space include:

Holicity Inc (Ticker: HOL) merging with small satellite launch provider Astra

New Providence Acquisition Corp (Ticker: NPA) merging with space-based cellular broadband provider AST Space Mobile

Osprey Technology Acquisition Corp (Ticker: SFTW) merging with geospatial intelligence company BlackSky

Vector Acquisition Corp (Ticker: VACQ) merging with satellite launch provider Rocket Labs

NavSight Holdings (Ticker: NSH) merging with space data collection company Spire

This article will take a deep dive into these five companies to examine which of these provide the best risk/reward opportunity for investors

Astra/Holicity (HOL):

Astra is a small satellite launch provider with the mission of offering frequent rocket launches into space. While companies such as Space X and Blue Origin aim to transport people and large amounts of goods, Astra’s goal is to build smaller rockets that can be launched from anywhere.

Astra has two core services:

They want to provide orbital deliveries to sun-synchronous and low inclination destinations

They want to provide dedicated launch services of 50kg - 100kg payloads starting in 2021 and 2022.

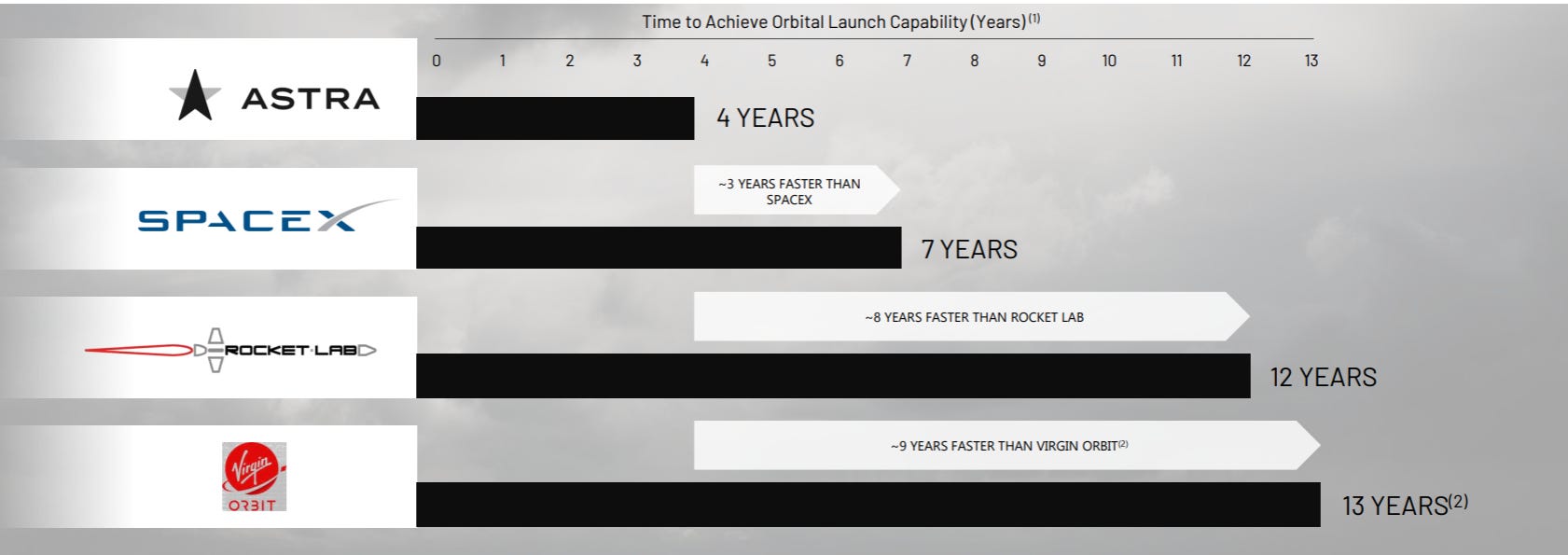

Astra has one of the fastest iteration timelines out of any space company. The company was started in 2016 and was already testing its first Rocket 1.0 by 2017 and had competed in the DARPA (Defense Advanced Research Projects Agency) challenge by 2020.

In September of 2020, the company made its first orbital launch attempt and demonstrated launch capability by December of that year.

In addition to having a fast timeline, Astra has one of the best management teams out of any space company. Astra also falls in the category of founder-led companies, which is always a nice signal for investors.

Their CEO and co-founder Chris Kemp was the former Chief Technology Officer of NASA and previously co-founded OpenStack. The other co-founder and currently Astra’s CTO Adam London previously led major rocket initiatives at DARPA and NASA and has 4 years of management consulting experience at McKinsey&Company.

Their Chief Engineer Chris Thompson and VP of Manufacturing Bryson Gentile are both ex-Space X employees and their CFO Kelyn Brannon was the former Chief Accounting Officer and VP of Finance for Amazon.

Astra’s production goals for the next few years are to build out its rocket factory by the end of 2021 and scale up its factory operations through 2022 and 2023. They have ambitious goals of facilitating monthly launches by 2022.

In the latter half of 2023, Astra wants to begin providing spaceport services to help anyone launch rockets into space. Additionally, they also plan on building out their modular spacecraft platform in 2023, which they claim will substantially increase their revenue growth.

Astra’s biggest competition is Rocket Labs, another company that is also aiming for smallsat launches and has already reached orbit. Rocket Labs currently has a definitive deal agreement with Vector Acquisition Corp to go public and will be discussed in more detail in this article.

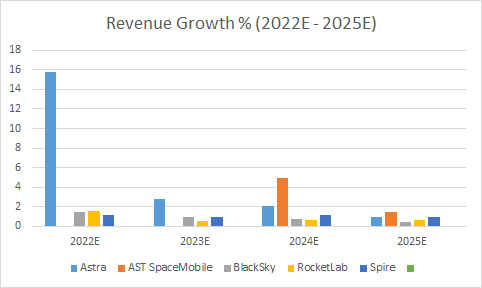

In terms of financials, Astra is still a no-revenue company that has plans on ramping up its productions in the next 5 years. They claim that they can grow revenues from $4 million in 2021 to $67 million in 2022, suggesting a 1700% growth over just one year.

By the year 2025, Astra is projecting roughly $1.5 billion in revenue with a 70% gross margin and 46% EBITDA margin. Their cash flows are also projected to increase significantly over the period as they reduce their CAPEX requirements each year.

Given the enterprise value of $2.1 billion, Astra is currently being valued at 3.1x their 2025 EBITDA projection and 1.41x their 2025 revenue projection. The merger with Holicity will provide the company with $489 million in cash, which will help with the production of their Rocket 3.2 and Rocket 3.3 launch.

AST Spacemobile/New Providence (NPA):

AST SpaceMobile is targeting the global mobility market with the goal of eliminating coverage gaps and enabling billions of people to stay connected through their mobile phones.

According to AST SpaceMobile, 51% of the world’s population currently live without broadband coverage with 5 billion mobile phones going in and out of coverage at any point. SpaceMobile aims to solve this problem by creating a space-based cellular network that will provide coverage anywhere at any time.

The biggest bull case for SpaceMobile comes from the $1 trillion TAM or total addressable market. As of now, 3.3 billion phones around the world are not connected to cellular broadband, and another 0.7 billion having no coverage at all.

SpaceMobile plans on being compatible with all 5 billion phones around the world, giving the company a massive opportunity to disrupt broadband and bring affordable service to people in equatorial regions with limited connections.

Given the size of this market, SpaceMobile sits in a very favorable position. They have claims on over 750 patents on their broadband technology and have commercial agreements with major household brands such as Vodafone, Rakuten, and AT&T.

While Elon Musk’s Starlink poses a potential challenge to the company, the key difference is that Starlink will be selling its own satellite dish and router to its customers. On the other hand, SpaceMobile doesn’t have the hurdle of selling any hardware at all.

In fact, the introduction of Starlink may be a potential catalyst for AST SpaceMobile. If traditional network providers such as Verizon and T-Mobile want to compete with Elon Musk, they will most likely have to rely on SpaceMobile to provide an alternative to their customers.

Abel Avellan, the CEO and Chairman of AST SpaceMobile, was the former founder of EMC (Emerging Market Communication), which sold for $550 million in 2016. He has 25+ years of experience in this industry with over 18 patents to his name. Tom Severson, the COO and CFO of AST SpaceMobile, previously worked with Abel Avellan at EMC as the former CFO. The fact that both of these executives have joined together on another project is always a good sign.

SpaceMobile’s Chief Technology Officer Dr. Huiwen Yao has 30+ years of experience in engineering satcoms and was previously at Northrop Gunman working on innovation systems. Chris Ivory, the Chief Communication Officer, was also at EMC prior to SpaceMobile.

Phase 1 of AST Spacemobile’s plan aims to deliver the service to roughly 1.6 billion people living in equatorial regions in 2023, with subsequent plans of extending service to Europe and North America. According to their investor presentation, they plan on using the cash flows from Phase 1 to deploy additional satellites all over the world.

The business model of the company is based on a 50/50 revenue share model where direct customers and partners split the cost. The projections of the company are based on a 4 year ramp to reach low to middle single digit penetration and low double digit penetration afterward.

In terms of financials, the SPAC deal values AST SpaceMobile at $1.8 billion at $10/share. SpaceMobile will receive $423 million in proceeds from the transaction, most of which is going to be used to fund their first phase commercial launch in 2023.

Out of all the other space companies in this analysis, AST SpaceMobile has aggressive growth estimates with almost 491.2% revenue growth projected from 2023 to 2024. Their EBITDA margin will be negative for the next 2 years in 2021 and 2022 due to lack of revenue and investment in the company but is projected to improve significantly starting in 2023.

At the current enterprise value of $1.39 billion, SpaceMobile is trading at a 2023 revenue multiple of 7.69x and a 2025 revenue multiple of 0.53x. The EBITDA multiple is 10.71x their 2023 estimates and 0.54x their 2025 estimates.

If these projections are correct, AST SpaceMobile is the best value play out of all the space SPACs currently in the market. However, it is important to note that this company is still pre-revenue with a very ambitious growth model.

AST SpaceMobile, therefore, seems to be a hit or miss company. If their product timeline comes to fruition, the stock price could easily 20-50x. Given the fact that they already have key commercial partnerships and investors involved, I am optimistic about the company’s future.

BlackSky/Osprey Technology (SFTW):

BlackSky is a geospatial intelligence company focused on disrupting spatial imagery and space-based data and analytics. The company is a first-mover in real-time Earth observation and has ambitious goals of accelerating satellite constellation, sensor networks, software application development, and commercial go-to-market.

Blacksky’s business model involves 3 core services:

High-frequency satellite imagery with dawn to dusk autonomous tasking. This service will be offered as a multi-year contract and is expected to make up roughly 64% of future revenue for the company. The gross margin for this service is expected to be 90%.

Site monitoring and analytics software that will be sold in a SaaS-like model. This will create recurring revenue for the company and is expected to make up 33% of expected revenue with 60% gross margins.

Operational and engineering solutions catered for government customers that will make up the remaining 3% of expected revenue with a low gross margin of 10%. This service will be sold through fixed-price contracts.

Blacksky wants to put 23 low-cost and high revisit small-sats on-orbit by 2023 with the aim of providing real-time sensor agnostic data and analytics to its customers. The total addressable market of the real-time Earth observation industry is estimated to be roughly $40 billion.

While the space image capturing market is currently dominated by legacy satellite companies, BlackSky prides itself on being able to provide a better quality service for only 10% of that price.

BlackSky’s technology stack is also arguably the best out of all legacy satellite players, with artificial intelligence capabilities in distinct areas such as event detection, computer vision, routing prediction, and time-series analysis. All of these provide the company with proprietary data that gives BlackSky a massive competitive advantage.

Moreover, BlackSky is better vertically integrated when compared to all of its competitors. While legacy players will purchase satellites from manufacturers, BlackSky owns a 50% stake in LeoStella JV - one of the leading constellation construction and smallsat production companies.

BlackSky already has contracts in place which could potentially be worth $630 million. Some of their key partners include the U.S Army, the U.S AirForce, and the National Reconnaissance Office, which is responsible for all satellite intelligence of the U.S Government.

While BlackSky is mostly partnered with U.S government agencies as of now, it has plans of expanding into emerging markets and the commercial industry starting from 2025. Some of the commercial uses of BlackSky’s service include pipeline and inventory monitoring, insurance property assessments, mining surveillance, agricultural crop health monitoring, and so on.

The company’s management team is also top-notch with years of experience in the industry. BlackSky’s CEO Brian O’Toole is a serial entrepreneur whose last business OpenWhere was acquired by Blacksky itself. He worked as the Chief Technology Officer of the company for 4 years before moving up to the position of CEO.

BlackSky’s current CTO Peter Wegner was the former Chief Technology Officer of SpaceFlight Industries and has a Master’s Degree in AeroNautical Engineering from Stanford University. Their COO Nicholas Merski was the previous Engineering Division Chief of the United States Air Force and their CFO Brian Daum was the previous CFO of MotionSoft, Savi Technology, and Centrifuge Systems.

In terms of financials, BlackSky is going public with a Pro-forma enterprise value of $1.1 billion with $318 million of cash in trust. The company is expecting aggressive revenue growth over the next 5 years with positive EBITDA starting from 2022.

The company’s gross margin is expected to improve significantly over time as they roll out more smallsats in orbit and introduce their developer APIs to promote their software analytics platform.

At a share price of $10, the company is valued at 24x their expected 2021 revenue and 2.03x their expected 2025 revenue. If BlackSky’s estimates actually come to fruition, SFTW poses a very attractive investment opportunity that can potentially 5-10x in the long-term.

Given the company’s product map and timeline, BlackSky is ahead in product-market fit when compared to the other recent SPACs in the space industry. The company looks promising with important contracts already in place and a strong management team that knows how to navigate the industry.

However, the current multiples of this company are based on a peer group of data analytics companies such as Snowflake, Palantir, and DataDog, and it will be a challenge for BlackSky to prove whether they really belong in this set. Therefore, the BlackSky software analytics platform will be the segment that every investor will be watching for the next few years.

The SaaS-like model of that product can create significant recurring revenue and predictable cash-flow for BlackSky, and take the company’s stock from being a speculative investment to one that investors can better understand. For now, BlackSky is still an uncertain company with a high risk/reward profile.

Rocket Lab/Vector(VACQ):

Rocket Lab is a vertically integrated provider of small launch services, satellites, and spacecraft components. Their business model involves delivering end to end solutions in three key areas:

Launch of small and mid-sized services

Manufacturing satellites and other space systems

Building space applications

In many ways, Rocket Lab is simply a smaller Space X and is one of the only two private companies that have delivered regular and reliable access to space. Over the course of just 6 years, Rocket Lab has had 18 launches and has deployed over 97 satellites to orbit.

Rocket Lab was the first company to build a 3D printed rocket engine that is fully carbon composite and is the only manufacturer of reusable small launch vehicles in space. They also own the first and only private orbital launch site in the world.

The most unique aspect of Rocket Lab’s technology, however, is that their rockets can convert into satellites in orbit. This presents a very lucrative opportunity for the company since they can leverage this to not only provide smallsat launches but also satellite services in the future.

In April of 2020, Rocket Lab acquired satellite hardware manufacturer Sinclair Interplanetary, making the company vertically integrated from start to finish. The company has also won multiple successful contracts, such as the NASA Capstone Mission to the moon and the NASA Propellent Depot Mission in LEO.

Rocket Lab’s launch service has scaled to monthly cadence faster than any other private company. With over 18 launches, Rocket Lab is far ahead of its competitors in smallsat launches. Their customers include NASA, DARPA, United States Space Force, BlackSky, and Spire. Roughly 50% of their customers are commercial, while the rest are split between civil and defense organizations.

Their rocket, named Electron, uses extensive automation and 3D printed parts with 90% of the production completed in-house. Rocket Lab’s next plan in launch services is to create a mid-sized rocket, named Neutron, which can carry constellations to space.

By 2028, 83% of all smallsat launches are expected to be constellations, and Rocket Lab estimates that it will be able to lift 98% of all satellites forecasted to launch through 2029. The Neutron will be a much more direct alternative to SpaceX’s Falcon Rocket with the first launch expected in 2024.

Rocket Lab’s satellite service, known as Photon, offers services both in LEO and deep-space missions. The Photon service means that customers no longer have to build their own satellite and can instead buy a launch and orbit management system directly from Rocket Lab.

In terms of management experience, Rocket Lab’s CEO Peter Beck never attended university and instead gained engineering experience from working at Industrial Research, now Callaghan Institute. In 2016, Peter Beck was named EY Entrepreneur of the Year.

Rocket Lab’s CFO Adam Spice has previous work experience at Intel and Broadcom and was the previous CFO of MaxLinear. Rocket Lab’s VP of Launch Shaun D’Mello was an engineer at CRC-ACS prior to joining the company.

Based on the price of $10/share, Rocket Lab is currently being valued at an EV of $4.08 billion. This is roughly 5.4x their 2025 expected revenue and 24x their 2025 expected EBITDA. Rocket Lab is expected to be cash-flow positive for the first time starting from 2024.

The revenue growth projections are still extremely aggressive with almost 155% growth in 2022 and about 50-60% growth from there on after. The company is expected to generate positive EBITDA for the first time in 2023.

Given all of this information, Rocket Lab is a much safer bet when compared to Astra or AST SpaceMobile. They have key contracts in place with a proven track record of delivering on their promises. They are far ahead of Astra or Virgin Orbit in terms of the product timeline and are only lagging Space X in this area.

However, the most concerning news for Rocket Lab would be if Space X entered the smallsat launch industry. Currently, Space X’s Falcon only deals with large deliveries, and customers have to rideshare with other companies to send their satellites to orbit.

Rocket Lab, on the other hand, allows its customers to control the schedule for launches and the destination of the orbit. This has allowed Rocket Lab to create a niche market for itself where they are able to serve small deliveries into space.

Space X does have the engineering team and capabilities to enter the smallsat launch industry if they want to, although that is not exactly what Elon Musk is focusing on as of now. The goal for Rocket Lab should be to innovate as fast as possible to establish itself as a key player in small and medium-sized deliveries before Space X makes any strides in this market.

Overall, I believe that Rocket Lab is perhaps the best space investment available in the public markets, and it is where all my money would go if I could only invest in one.

Spire/NavSight(NSH):

Spire is a space-based data analytics company that operates with a recurring revenue business model. The company collects space data through LEMUR, or Low-Earth Multi-Use Receiver, nanosatellites and delivers this data to customers for a subscription. Their software analytics platform SpireSight offers analytics, insights, and other predictive tools through an API to clients.

The company primarily operates in 4 distinct areas:

Maritime: Space-based ship monitoring

Aviation: Space-based aircraft monitoring and route optimization

Weather: Predictive analytics for weather forecasting

Orbital Services: Infrastructure to provide “space-as-a-service

The space-based analytics industry currently has a total addressable market, or TAM, of roughly $66 billion. The biggest growth opportunity here lies in weather forecasting as climate change is expected to increase weather variability by almost 60% by 2050. This means that many industries, such as agriculture and aerospace, are going to have to rely on analytics services such as Spire in order to avoid economic loss.

In terms of competitive advantages, Spire’s LEMUR nanosatellites are built in-house, making them vertically integrated. It reduces the costs for the company while also making production much faster. Since 2016, Spire has launched 141 nanosatellites. While the development cycle for most legacy data providers is 3-5 years, Spire has reduced the development cycle to just 6-12 months.

Spire’s data is real-time with global coverage, even in areas with remote reach. Since Spire uses an API to deliver data to customers, it can be easily integrated into the technology stack of its clients. Some recent customers of Spire include NASA, Chevron, and the U.S Coastal Guard.

Spire plans to expand into collecting data sets on soil moisture, Ionosphere, Microwave Sounding, and Spectrum monitoring in the future, which will allow the company to penetrate various different industries. Spire also plans on expanding into the Middle East and Latin America in the next 5 years, which are both largely underserved markets today.

Spire’s CEO Peter Platzer has previous experience at Deutsche Bank and Boston Consulting Group and is an alumnus of Harvard University. Their Chief Financial Officer Tom Krywe has previously worked as a VP of Finance at Jive Software and Senior Director of Finance at EMC. Jeroen Cappaert, Spire’s Chief Technology Officer, was previously a CubeSat researcher at NASA.

The transaction with NavSight values Spire at an Enterprise Value of $1.2 Billion with $230 million left in trust. The company also received PIPE commitments of about $245 million through the transaction.

Spire is projecting aggressive revenue growth between 90% - 110% each year between 2021 to 2025. They are expected to become EBITDA positive starting in 2022. If these projections hold true, Spire will be one of the fastest companies to hit $100 million in ARR.

Due to the recurring revenue model, Spire will maintain strong gross margins throughout its growth trajectory. While CAPEX will a large portion of revenues early on, they are projecting expenditures to be just 3% of ARR by 2025.

In conclusion, I personally believe that Spire is being too aggressively valued by investors. The multiples of this company are based on a peer group of vertical SaaS players such as Shopify, Datadog, and Palantir. However, the key difference is that these companies are already well established and operate within a proven market.

The Space-as-a-Service industry is still in its infancy with lots of competitors. Spire doesn’t have an actual moat other than its vertical integration and doesn’t have nearly the same brand and name recognition that the companies within its peer group carry.

The real investment thesis for Spire is based on the fact that the company has an ARR business model, which makes it attractive as a high gross margin play. If Spire does become successful, it will be able to scale at an extremely fast rate, but for now - the risk/reward is simply not good enough for my personal taste.

Concluding Thoughts:

Based on current financials, NPA/AST SpaceMobile provides the best risk/reward opportunity amongst Space-related SPACs. Although the EV/Revenue multiple is the highest for this SPAC, the risk could be well worth it if the company’s projections come true.

For investors who are looking for a more reliable investment, VACQ/Rocket Lab presents the most attractive investment opportunity since they are the furthest along in terms of product and have reasonable expectations of future growth.

However, it is important to note that almost all of these SPACs are valued aggressively based on expected earnings that we have not seen yet. There is a high probability that none of these companies are able to establish a dominant market position, and are acquired by larger players, or worse, forced to file for bankruptcy.

Investing in any of these SPACs still remains a gamble more than an investment as of today.