Defensive Hedging as a Strategy

How Bill Ackman's Hedge Fund Protects and Magnifies Returns Through Defensive Hedging

Hedging is a risk management strategy employed to offset losses by taking an opposite position in a related asset. Typically, hedging strategies will employ some form of derivative financial instrument, such as options or futures contracts. During turbulent times in the market such as the one we are in today, hedging can be one of the best ways to protect your portfolio.

“During turbulent times in the market such as the one we are in today, hedging can be one of the best ways to protect your portfolio”

Effective hedging, however, is not easy. Hedging does reduce downside exposure, but it also comes at the risk of limiting upside potential. There is also an inherent risk in hedging for investors who don’t understand the financial instruments involved in the process.

So to get a better understanding of how to effectively hedge downside risk, we decided to do a deep dive into Pershing Square’s track record with defensive hedging. Over the years, Ackman’s hedge fund has made some incredibly successful and lucrative downside bets that have increased investor returns. We wanted to get an idea of Ackman’s hedging strategy, as well as the financial instruments he utilized in each of them.

Hedging Bet #1

Time Period: 2005 - 2009 (CDS Hedge)

Investment Cost: $64 million

Total Proceeds: $1.2 billion

Multiple of Capital (MOC): 18.5x

Financial Instrument Used: CDS on Bond Issuers (mostly MBIA)

In 2002, Bill Ackman published a report underlining his short thesis on Municipal Bond insurer MBIA. The report, which was titled “Is MBIA Triple A?”, provided details on the enormous leverage that was hidden inside MBIA and its subsidiary MBIA Insurance Corp.

Ackman’s short thesis was based on the following factors:

Municipal Bond Insurance is not a lucrative business model, given that muni-bonds generally have guarantees from the state. Even then, insurance is generally used to lower the interest rate on these bonds. As a result, these insurance premiums were eating into the public money

MBIA’s accounting was fraudulent and didn’t reflect the risk factors, particularly tied to leverage

The structured finance products of MBIA were suspect. MBIA aimed to guarantee AAA-rated CDOs, but Wall Street and MBIA was manufacturing these ratings

The loss of AAA rating would significantly impact MBIA’s ability to remain solvent

Not surprisingly, the report was met with resistance and doubts from all over Wall Street. Before the report was even published, MBIA’s Chairman and CEO Joseph Brown privately met with Ackman. This is what he had to say:

“You’re a young guy, early in your career. You should think long and hard before issuing the report. We are the largest guarantor of New York state and New York City bonds. In fact, we’re the largest guarantor of municipal debt in the country. Let’s put it this way: We have friends in high places.”

Ackman didn’t step down. He hired a top forensic accounting expert and brought evidence of MBIA’s fraudulent accounting several times to Moody’s. In 2005, Ackman wrote a letter to Moody’s Board of Directors which read:

“Moody’s AAA rating is so powerful and credible that investors don’t do any due diligence on the underlying credit. Every day that Moody’s incorrectly maintains an AAA rating on MBIA, these extremely risk-averse investors unwittingly buy bonds that are not deserving of Moody’s AAA rating.”

In addition to shorting the stock of MBIA, Ackman also purchased CDS, or Credit Default Swaps on MBIA’s debt. These swaps act as insurance in the case of credit events or solvency risks that the issuer of the debt may face. In exchange, the buyer is forced to pay annual premiums to the seller.

The premiums that Ackman paid on his MBIA CDS position put a massive drag on his overall returns for many years. Finally, in February of 2008, MBIA cut its dividend and suspended its structured finance activities. In June of the same year, MBIA and Ambac, the two largest municipal bond insurers, lost their AAA rating from Moody’s, and Ackman walked away with $1.2 billion of proceeds from the trade.*

This particular bet showed Ackman’s conviction in his position, despite having dealt with criticism and drag on returns for many years. As Whitney Wilson, Co-Manager of T2 Partners, put it:

“For five years he was wrong, wrong, wrong. Then he made billions… He is the most relentlessly stubborn person on the planet.”

To read more about the MBIA trade, check out the book Confidence Game: How a Hedge Fund Called Wall Street’s Buff by Christine Richard

* = Ackman owned smaller positions of CDS on other insurers such as Assured Guaranty, Ambac, PMI Group, XL Capital Insurance, Financial Securities Assurance, and Radian Group

Hedging Bet #2

Time Period: 2020

Investment Cost: $27 million

Total Proceeds: $2.6 billion

Multiple of Capital (MOC): 96.3x

Financial Instrument Used: Index CDS on Investment Grade and High Yield Bonds

After a few years of underperformance relative to the S&P due to positions such as Herbalife and Valeant Pharmaceuticals, Bill Ackman entered the financial limelight once again in 2020.

In February of 2020, Ackman began to worry about a pandemic related economic recession. His hedge fund bought insurance policy through CDS on almost $71 billion worth of corporate debt, including $44.5 billion of U.S investment grade bonds, $23.1 billion of an equivalent European index, and a $3.1 billion notional exposure to Europe’s high yield debt.

This bet was risky, to say the least, and required an enormous level of conviction due to the volatility it imposed on the fund’s portfolio. At its peak, this one position accounted for almost 40% of Pershing Square’s entire AUM. On March 13, when the S&P jumped 10%, the value of the contracts had dropped by $800 million in just one day.

By the time Ackman appeared on CNBC on March 18, he had sold about half of the defensive hedge position. He then went on to use the proceeds to buy into many of his existing positions, while also adding a new position in the coffee chain Starbucks. As of March 31, Pershing Square had not only offset all the loses on their long-equity positions, but had actually ended the quarter with substantial gains relative to the S&P.

One of the underappreciated aspects that allowed Ackman to pursue such a bold strategy lies in the unique structure of his hedge fund. In 2014, Pershing Square publicly listed itself on the Euronext Amsterdam - the Netherlands stock market. So while a lot of hedge funds were facing capital calls from investors during the pandemic related scare, Ackman had the resource of permanent capital. It is safe to say that he made good use of this opportunity.

Hedging Bet #3

Time Period: Late 2020 - 2022 (Ongoing)

Investment Cost: $188 million

Total Proceeds: $1.4 billion

Multiple of Capital (MOC): 7.4x

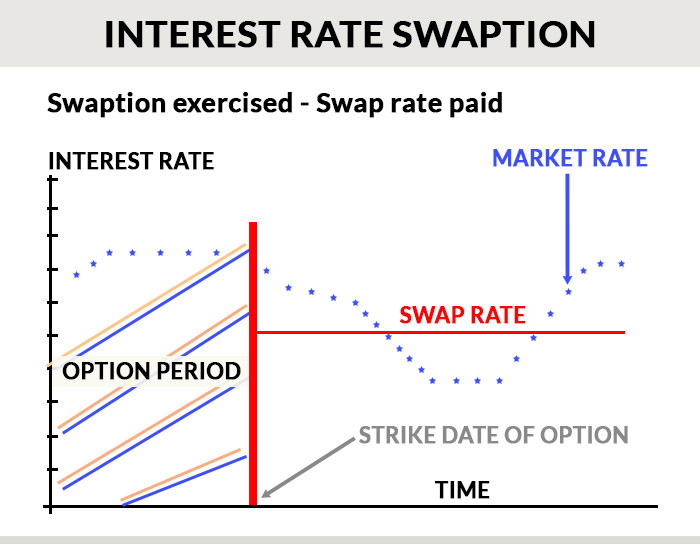

Financial Instrument Used: OTM 2Yr and 10Yr Swaptions

Towards the end of 2020, Pershing Square came to the conclusion that interest rates would substantially rise throughout the next few years. The thesis for this position was fueled by the policy decisions of the Federal Reserve and the U.S government.

As of December 2020, the unemployment rate was nearly 6.7% with CPI inflation at 1.4%. Due to QE and stimulus, Ackman was expecting both metrics to take substantial turns for the rest of 2021. By the end of 2021, this prediction turned out to be right, with unemployment falling to 3.9% as of December 2021 and CPI inflation ramping up to almost 7.0%.

To hedge against interest rate risk, Pershing Square purchased out-of-the money interest rate swaptions starting towards the end of 2020. In January of 2021, they sold nearly 90% of the market value of the position, generating about $1.25 billion in proceeds. Since then, they have replaced this hedge with additional longer dated out-of-the money swaption.

Swaptions, which stand for swap options, is a type of option contract which gives the buyer the right to enter into a swap contract on a specified date. These options are generally purchased in the over-the-counter market, and are not traded on an exchange. This requires both the buyer and the seller to mutually agree on the notional amount, time period, and the fixed/floating rates involved with the instrument.

Swaptions come in two forms: payer swaptions and receiver swaptions. The payer swaption gives you the right to pay a fixed rate and receive a floating rate of interest, usually the LIBOR rate. On the other hand, a receiver swaption is exactly the opposite.

To use an example, a borrower with loans maturing sometime within the next year might want to purchase payer swaptions to hedge against any substantial interest rate movement. If the variable interest rate, which is tied to LIBOR, moves above the fixed interest rate that was agreed upon, then the borrower would want to exercise the contract to pay the fixed rate instead.

Here is an illustrative chart that shows the return profile of a swaption contract

One of the interesting characteristics of this interest rate hedge was the asymmetric payoff structure that Pershing Square was able to create for itself. The table below shows the hypothetical effects of a reasonably possible percentage change to the rate (as of the end of 2020):

Takeaways and Lessons

From studying Bill Ackman and Pershing Square’s track record of defensive hedging, there were 3 main lessons that we walked away with:

Only take bets in which you have large convictions. The market will often remain irrational longer than you would expect, or longer than you can remain solvent in many cases.

Look for bets with asymmetric payouts. This means limited upfront carrying costs and investments with opportunities to generate large multiples on your capital. This also means investments with limited downside in cases where the potential risk does not transpire

Hedging is more lucrative on a short term basis where the monetization of it can become a funding source for cheap equities during downturns. Continuous hedging strategies do work, but it will often put a drag on overall returns.